Take the faster path to growth. Get Smith.ai today.

Affordable plans for every budget.

Funding can support purchasing more equipment, increasing store space, hiring more staff, or refinancing existing loans. Business loans are useful funding sources since the rates are typically better than adding debt to credit cards. Small business owners can also keep control of their business without sharing profits or decision-making capacity with investors.

Finding the right business loan for your small business can feel like an overwhelming experience. But it doesn't have to be! This guide will provide you with all the information you need to get the right business loan. From types of loans and highly rated banks to questions to ask when getting a loan, you'll be equipped with successfully securing the funding your business needs to fuel growth.

Before diving into information about small business loans, it's important to understand the common terminologies. Here is a list of common business loan terms and their definitions.

● Loan term: The stated period the borrower will make payments on the loan. Loans can vary in length, such as four, five, ten years, or more.

● Principal: The amount of money that is being borrowed, excluding any fees or interest payments.

● Interest: The amount charged for borrowing funds. Interest is usually a percentage of the principal and expressed as an Annual Percentage Rate (APR).

● Annual percentage rate (APR): Reflects the interest cost and fees charged on the loan as a yearly rate.

● Interest-only payments: Payments made on the loan cover only the interest without paying the principal loan amount. Borrowers will have to refinance or pay back the principal as a lump sum at the end of the loan term.

● Revolving terms: Associated with credit lines or credit cards, the account can be used and paid down repeatedly within the credit limit.

● Overdraft: Occurs when a borrower withdraws more money from a bank account than what the account holds.

● Asset: A tangible item with value that the borrower owns and can use as collateral.

● Collateral: An asset offered by the borrower to secure a loan. If the borrower defaults on the loan, the lender can acquire the asset(s).

● Default: The failure to make payments on the loan as agreed upon during the loan approval.

● Liability: Debts or obligations a business can resolve through periodic payments or transfer of goods and services.

● Accounts payable: Also referred to as "current liability." A short-term debt you need to pay off.

● Accounts receivable: Payments someone owes you, such as outstanding invoices.

● Debt financing: A loan or any method to finance your business where you will have to repay the principal plus interest.

● Maturity: Your loan reaches maturity when you make your last payment paying off the entire principal and all interest.

● Refinancing: The process of paying off an existing debt or loan with a new loan with better terms and interest rates.

● Origination fee: A fee lenders charge up front to process a new loan application.

Suppose you are deciding between a business loan, getting credit cards, or seeking capital investors. In that case, it's good to understand the benefits loans offer compared to alternative funding sources.

Business loans offer a short-term increase in cash flow or help cover equipment or salaries for additional hires your business needs for growth. Depending on the loan, it can take five to ten days for a loan application to process. In contrast, networking for funds from venture capitalists could take as long as a year.

Investors providing capital often also want a say in how the business is run and how the funds are used. Most business loans or lines of credit won't dictate how you use your funds once you qualify for them. Thus, you are to keep control of your operations and not have to share potential profits.

While credit cards offer both the benefits above, the interest rates are usually higher. Depending on the type of loan and repayment terms, you are most likely to get a business loan with better interest rates.

There are plenty of funding sources for small businesses, with the most popular ones coming from banks in the form of a bank term loan. However, there are other types of loans that exist for small business owners.

Here is information on six common types of business loans, what they mean, and the pros and cons for each:

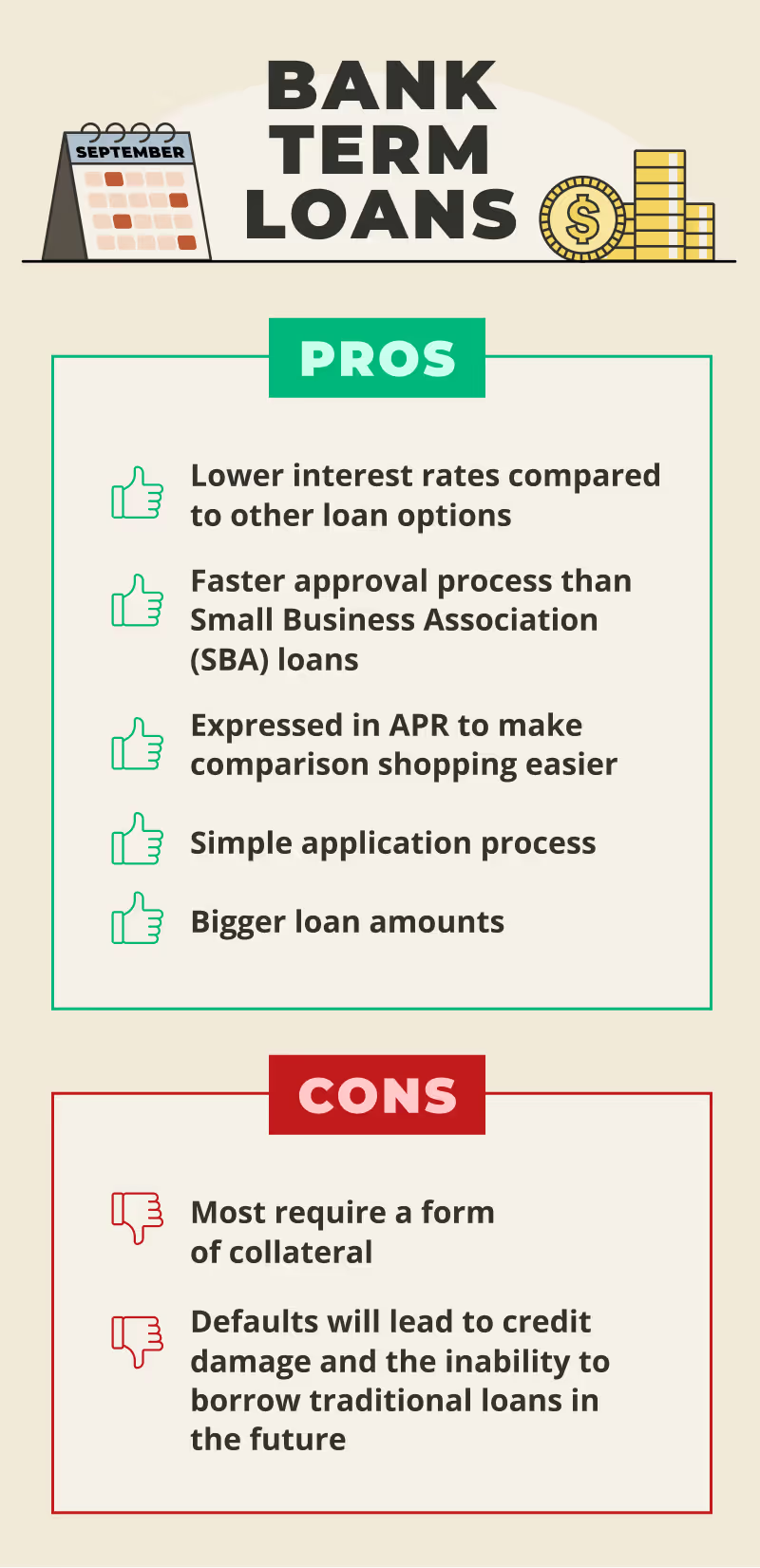

The most common type of small business loan is a traditional term loan from a bank. They are set amounts of funding you repay according to a fixed schedule. It's best to use these loans for significant purchases, such as vehicles, software, real estate, or equipment.

These types of loans work similarly to how a car loan or home mortgage does. They include a combination of interest and principal payments, where the beginning of the loan term is mostly paying interest, and towards the end of the term, you pay more principal. Depending on the bank, you can also pay loan fees upfront or include them in the loan balance.

The interest rate you are charged on bank term loans will vary depending on the:

● Current index rate

● Length of the loan term

● Perceived credit risk of the borrower

Pros

● Lower interest rates compared to other loan options

● Faster approval process than Small Business Association (SBA) loans

● Expressed in APR to make comparison shopping easier

● Simple application process

● Bigger loan amounts

Cons

● Most require a form of collateral

● Defaults will lead to credit damage and the inability to borrow traditional loans in the future

You are likely to find favorable loan terms when you apply for an SBA loan. The SBA acts as a middleman guaranteeing to lenders that borrowers will repay the loans. There are multiple loan programs available through the SBA, each designed for different types of businesses and with its own requirements.

The three main types of SBA loans for small businesses are:

● 7(a) loans: Capped interest rates, limited fees, and guaranteed amounts

● Microloans: Small loans of $50,000 or less to help with startup and expansion costs

● 504 loans: Fixed-rate, long-term financing for purchasing or repairing assets such as equipment, real estate, or machinery

Pros

● SBA offers a government guarantee covering 75% to 90% of the loan

● Long repayment times

● Reasonable interest rates

Cons

● Lots of paperwork involved

● Takes longer to get approved

● Typically has strict requirements to qualify

If you need a short-term money solution to fund your business, banks and alternative lenders provide working capital loans for this purpose. Unlike most loans, you don't need to identify the purpose of the loan, as it is intended to help you with short-term cash flow issues or investment needs.

Working capital loans can be used for anything related to your business, including:

● Paying staff

● Purchasing stock

● Covering business operational costs

● Investing in growth

Pros

● Get cash flow to keep your operations running

● Gives you time to search for ways to increase revenue or secure long-term loans

● No restrictions on how the money is spent

● Can be secured or unsecured

Cons

● Higher interest rates

● Short repayment terms

A business line of credit is similar to a working capital loan, where you can get funds for day-to-day cash flow needs. However, the line of credit has longer repayment terms. The line of credit allows you to take only the money you need, and you will pay interest only on the amount you use.

There are requirements to qualify, such as:

● A credit score of at least 580

● Be in business for at least 12 months

● An average monthly revenue, such as $10,000

Pros

● Available for terms ranging from 90 days to several years

● Unsecured loans with no collateral requirement

● Gives you the ability to build your credit score

Cons

● Not recommended for larger purchases

● May come with additional fees for the credit

● Can risk your small business building up large debt amounts

Banks, the SBA, and other alternative lenders offer equipment loans and leases so your business can cover the costs of large equipment purchases. The equipment will act as the collateral of the loan. The loan or lease can cover:

● Office equipment, such as copy machines and computers

● Machinery

● Tools

● Vehicles

Pros

● The ability to make monthly payments on equipment instead of paying the full cost up front

● Easy and fast to obtain compared to other loans

● Preserves cash flow with low down payments

● May offer tax write-off benefits

Cons

● The terms of the loan sometimes outlive the equipment's useful life

● Interest rates vary widely by lender and can be fairly high

While there is no such thing as a 100% "unsecured" loan, unsecured business loans are named as such because they don't require you to provide any collateral, and approval relies heavily on your credit score.

However, be aware that some lenders will want you to provide a "personal guarantee" instead, meaning the lender can claim your personal assets if you default on the loan. This is why these loans are sometimes called personal loans or signature loans, even though the funds are intended for business purposes. Always make sure to read the fine print carefully, especially if a deal appears too good to be true.

Pros

● Access to cash for all business needs

● Shorter application process

● Doesn't require any collateral

Cons

● You need excellent credit scores to qualify

● Higher interest rates

● Lower loan amounts

● Often requires a personal guarantee

Besides the popular business loans previously mentioned, there are alternative routes to getting loans and funding besides from banks. You may want to consider these options if you haven't been in business for long or don’t have the strongest financial history.

Here are five of the less traditional or well-known funding sources that can support growth for your small business.

If you only need a small sum of up to $50,000, you may qualify for a microloan. These loans are typically offered by nonprofit organizations such as Accion and the SBA. Microlending especially prefers to fund minority-owned and women-owned businesses.

Peer-to-peer lending platforms match business owners with individuals who are willing to lend money for an interest rate. This method is different from an investor and similar to getting a loan from a bank, except you are in a contract with an individual.

Examples of these lending platforms include Lending Club, Kiva Zip, and Prosper.

While there tend to be higher interest rates and shorter repayment periods than traditional loans, online lenders offer business owners loans or lines of credit. You can easily apply online, get fast decisions, and have flexible lending criteria.

Examples of online lenders include PayPal, Kabbage, and OnDeck.

Although technically not a loan, a merchant cash advance is still a popular non-traditional way to secure funding for your small business. The funding provided is based on the amount of monthly credit card transactions your business makes while you repay the loan using credit card sales.

Your business receives an advance amount of money, typically up to 125% of your monthly transaction volume. While they are usually easy and fast to obtain, the interest rates can be as high as 30% a month.

Since most lenders prefer funding businesses that have been open for at least two years, the franchise startup loan is a great solution for anyone wanting to start a franchise without operation history. This loan is for anyone needing funding to:

● Use as working capital

● Pay franchise fees

● Build stores

● Buy equipment

While there are banks well-known for providing loans to small businesses, it's still good to know all the different options you have available. Contact multiple banks and compare offers to make sure you get the best possible terms for your loan.

Here are eight highly-rated banks to comparison shop with:

Although Wells Fargo's lending maximum is $500,000, it still offers various types of small business financing and lines of credit options. Their unsecured line of credit is also one of the most popular options since you don't have to put up collateral to qualify. They are also an active SBA 7(a) loan lender.

Wells Fargo's unsecured or secured credit lines range from $5,000 to $500,000. You will typically need at least $2 to 5 million annual sales to qualify. For credit lines:

● Up to $100,000, there are variable rates

● Over $100,000 in a one-year term

Other types of loans you can get through Wells Fargo include:

● Commercial real estate purchase loans

● Semi-truck financing

● Equity financing

● Loans for specific products to start or buy medical practices

Chase offers a variety of loans and financing options for small businesses. They are also a big lender of SBA loans, offering multiple types of SBA financing solutions, including:

● SBA 7(a) loans up to $5 million with flexible terms, longer maturities, and lower down payments

● SBA 504 loans up to $12.5 million with extended terms or competitive long-term interest rates available

● SBA Express loans and lines of credit up to $350,000 for faster funding

Other types of loans Chase offers include:

● Fixed and variable term loans starting at $10,000 with terms up to 7 years

● Small business loans of at least $5,000 with flexible terms from 12 to 84 months

● Equipment financing starting at $10,000 for up to 7 years of up to 75% of the equipment's useful life

● Commercial real estate loans starting at $50,000 with terms up to 10 years

One thing that makes Bank of America loans appealing is the reward opportunities they provide. When you meet certain account requirements, you can access benefits such as lower interest rates and no fees on wire transfers. If you are a service member or veteran business owner, you can also get a 25% discount on fees or loan administration.

Their term loans and lines of credit will typically require your business to have annual revenue of $250,000. Types of loans you can get through Bank of America include:

● Fixed-rate term loans of up to $250,000 with repayment terms up to five years

● Business line credits with no borrowing maximum and renews annually

● SBA 7(a) loans

● Business auto loans with a $10,000 minimum

● Commercial real estate loans with a $25,000 minimum

● Equipment loans with a $25,000 minimum

Although more well-known for their small business credit cards, Citibank also provides business loans and credit lines. They are great at curating their website for easy exploration. You can find a financing solution based on your business need, industry, or products and services.

Examples of their available loans include:

● Fixed-rate term loans range from $5,000 to $3 million, with terms up to 7 years, requiring a personal guarantee, and can be used for equipment

● Lines of credit ranging from $10,000 to $3 million, with variable interest rates and revolving terms

PNC offers some great loan options where you can apply online, through the phone, or in person. If you qualify, expect a simplified application and decision process as well as easy fund access. They offer:

● Unsecured term loans between $20,000 and $100,000 with fixed interest rates and terms up to 5 years

● Secured term loans between $100,001 and $3 million with fixed or variable terms up to 7 years

● Unsecured and secured credit lines at the same borrowing range of the term loans, and both have revolving terms and variable interest rates

● Auto loans ranging from $10,000 to $250,000 for terms up to 6 years

● Commercial real estate loans between $100,001 and $3 million with fixed or variable interest rates and terms up to 10 years

TD Bank is one of the best alternative banks providing various loan options for small businesses. They offer competitive interest rates and are known for excellent customer service. You can also expect no origination fees on loans under $100,000. However, they are only available in 16 states on the East Coast.

Types of loans offered by TD Bank include:

● Term loans between $10,000 and $1 million with terms ranging from 3 to 5 years

● Lines of credit between $25,000 and $500,000 with annual terms and no fees for credit lines under $100,000

● SBA 7(a) loans ranging between $250,000 and $5 million with terms up to 25 years

● SBA 504 loans ranging between $250,000 and $5 million with terms up to 20 years

Live Oak Bank focuses specifically on providing small business loans, including SBA loans, U.S Department of Agriculture loans, and commercial loans. They are considered the top lenders for SBA loans and provided $369,181,900 in 2020 to small businesses through 7(a) loans.

Their loans start at $150,000 and can be processed quickly online, including all required documents uploaded online. Their SBA loans have terms up to 25 years with the following maximums:

○ SBA 7(a) up to $5 million

○ SBA 504 up to $15 million

For another bank that specializes in SBA loans, you could also try Huntington National Bank. They offer a quick and easy online application process. You can apply within 10 minutes and get a fairly quick response. They also don't charge prepayment or application fees. A possible downside is they only serve in 11 states.

SBA loans offered through Huntington National Bank include:

● 7(a) loans to acquire, open or expand your business

● Express loans that have smaller maximum amounts but a faster review process

● 504 loans with long-term fixed-rate terms for equipment

● Life local business program newly established to support veterans, woman, and ethnically and racially diverse-owned businesses

Besides the banks listed above, there are other popular establishments to receive loans from. Here are the top three online lenders to consider.

The Biz2Credit platform has a wide range of loan options. They connect small businesses with lenders based on funding needs. While they aren't a direct lender and loan guidelines will vary, they do:

● Have a network of financial institutions as lenders

● Match you with the best loan options

● Offer loans up to $5 million

BlueVine is a lender that focuses on offering lines of credit to small businesses. They also have a checking account, online bill payment, and vendor program. While they don't lend to brand new startups, you can get a loan even with bad credit if you provide a personal guarantee. Features include:

● Business credit lines up to $250,000

● Invoice factoring with credit lines up to $5 million

● Disbursement of funds usually within 24 hours

For fixed monthly payments, check out the online lender Funding Circle. There are no annual revenue minimums for loans, and you can expect fund disbursement within 5 to 10 business days for SBA 7(a) loans. They also provide:

● Term loans of up to $500,000

● Minimum loan amounts of $25,000

● Loan terms ranging from six months to five years

Before jumping into applying for a loan, there are questions you should ask yourself and your potential lender to better understand what your business needs are.

Here are the top questions to consider before moving forward with getting a small business loan:

The top 10 questions to ask yourself when getting a loan are:

1. How much money do I need?:Business loans can range from several thousand to millions of dollars, so evaluate what expenses you might have.

2. What do I need the money for?: Think about what you need for your office space, equipment, employees, and marketing.

3. Do I expect my business needs to change during the period of the loan?: If you aim to hire more employees or reach a new audience, look into your lender’s policy to see how you can adjust your payment plan.

4. Have I been in business for at least two years? If not, would I rather wait?: If your business is under two years old, you might want to build your credit score before you apply for a business loan, as being a young company could give the lender license to charge you a higher interest rate.

5. What is the financial shape of my business?: Make a note of things that impact your financial health like: if you’re behind on rent for your office space, how much revenue your business is getting, or if you’re looking to expand your business in other areas, among other things.

6. What's my credit score?: Remember that having a credit score of 680 or higher helps you get a loan with a lower interest rate.

7. Do I have any outstanding loans?: Outstanding loans can hurt your credit score and having another loan can put more pressure on your business.

8. Do I want a short- or long-term loan?: Short-term loans are intended to be paid within a few months or a year, whereas long-term loans can take years to pay off. The higher the loan, the longer it take to pay back.

9. What collateral am I willing to pledge?: Personal real estate, cash from personal savings or business accounts, or are goods that your company hasn’t sold yet (accounts receivable) are all forms of collateral.

10. What is my cash flow, and how much do I have to cover any potential fees?: Consider how much money your company is making and create a budget plan that includes any potential fines or late fees.

The top 10 questions to ask your lender or bank when getting a loan are:

1. What kind of loan do you recommend for my business needs?: If your business offers a delivery service, the bank might recommend a loan for equipment.

2. How long will it take to pay back the amount I need?: Consider how many payments you want to make and an interest rate you’re comfortable with. These key factors will help you set up a payment schedule that is suitable for your business.

3. Does the loan require me to put up collateral or provide a personal guarantee?: Keep in mind that if you are unable to pay off the loan, the lender may go after your personal assets if you provide a personal guarantee.

4. How will my credit score impact my interest rates, and how can I reduce the interest rates?: The higher your credit score, the more reliable you are as a borrower. When you’re more reliable, the lower your interest rate may be.

5. What documents do I need before I apply?: It depends on the type of loan you’re applying for, but some staple documents you should have on-hand include your loan application, your business plan, tax returns and financial statements, and credit report.

6. How long does it take from application to funding if I am approved?: Again, depending on the type of loan you’re applying for, it can take up to several months.

7. What are the typical rates and closing fees for the type of loan I am considering?: Your lender, business needs, and whether you are applying for an SB or traditional bank loan will dictate your rate and closing fee.

8. What other annual or one-time fees are there?: An annual fee is a loan maintenance charge. You might pay other one-time fees like wire and lockbox fees.

9. Will I get ongoing support if my business needs change?: You might need to hire more employees than intended, create other departments, or pursue outside investments.

10. What does your loan renewal or modification process look like?: If you can’t make your payments every month, find out if they can provide you with short-term relief or impose any penalties.

Small business loans can help you retain complete control of your business and come with better rates than getting credit cards. To improve your chances of securing the best loan for your small business, there are several things you can do to prepare for a loan application.

Make sure you know your credit score and understand how your score can affect your interest rates. Typically, to get a loan with a good interest rate, your credit score should be at least 680. If you aren't at this number, there are ways you can improve your score before applying for a loan.

Examples include checking your credit report for errors you can remove and decreasing your credit utilization percentage.

Do you have any collateral you are willing to pledge for a loan? Collateral is something you offer as security for repayment of a loan. Banks like to know if you can afford to pay back a loan, if there is a situation where you can't, and how they will get their money back. The collateral pledged is the last resort option for banks to regain their money if you default on the loan.

Examples of assets you can use as collateral include:

● Property you or your business own

● Retail inventory

● Accounts receivable

● Business equipment

How long have you been in business? Banks typically prefer giving loans to businesses that have been operating for at least two years. It shows you aren't going to go out of business and lets you provide two years of essential documentation, such as profit and loss statements and tax returns, to prove your business is successful.

If you have not been operating for two years yet, you may want to consider alternative funding options and wait until you hit the two years before applying for a business loan from banks.

Lenders like to know you understand your business and have all the right documentation to support a low-risk borrower. Documents you should have in place and ready to show include:

● Business plan

● Financial history

● Expense sheet

● Financial projections for the next five years

Getting a business loan can fuel growth for your small business and allow you to fund strategies to attract more customers. More customers also mean you need a solution to maintain excellent customer service despite the increase in traffic to your business. The good news is, you don't have to do it all yourself, and services such as Smith.ai can help.

Smith.ai's virtual receptionists will support your small business with 24/7 website chat, after-hours phone answering, lead intake, appointment scheduling, payment collection, and more. We understand how valuable customers are, and regardless of how much funding you get and the growth you experience, keeping your customers satisfied is still paramount. While you spend time looking for funding and managing your growth, let Smith.ai take care of your customer service needs.

To learn more about how we can help you, schedule a free 30-minute consultation or dial (650) 727-6484. We even offer you a 30-day money-back guarantee. For any other questions, please send them to hello@smith.ai.

.avif)

Sean Lund-Brown is a current Marketing Assistant for Smith.ai. A graduate from Metropolitan State University of Denver, Sean graduated with a BA in Music and an individualized degree in Teaching Vocal Pedagogy.