Take the faster path to growth. Get Smith.ai today.

Affordable plans for every budget.

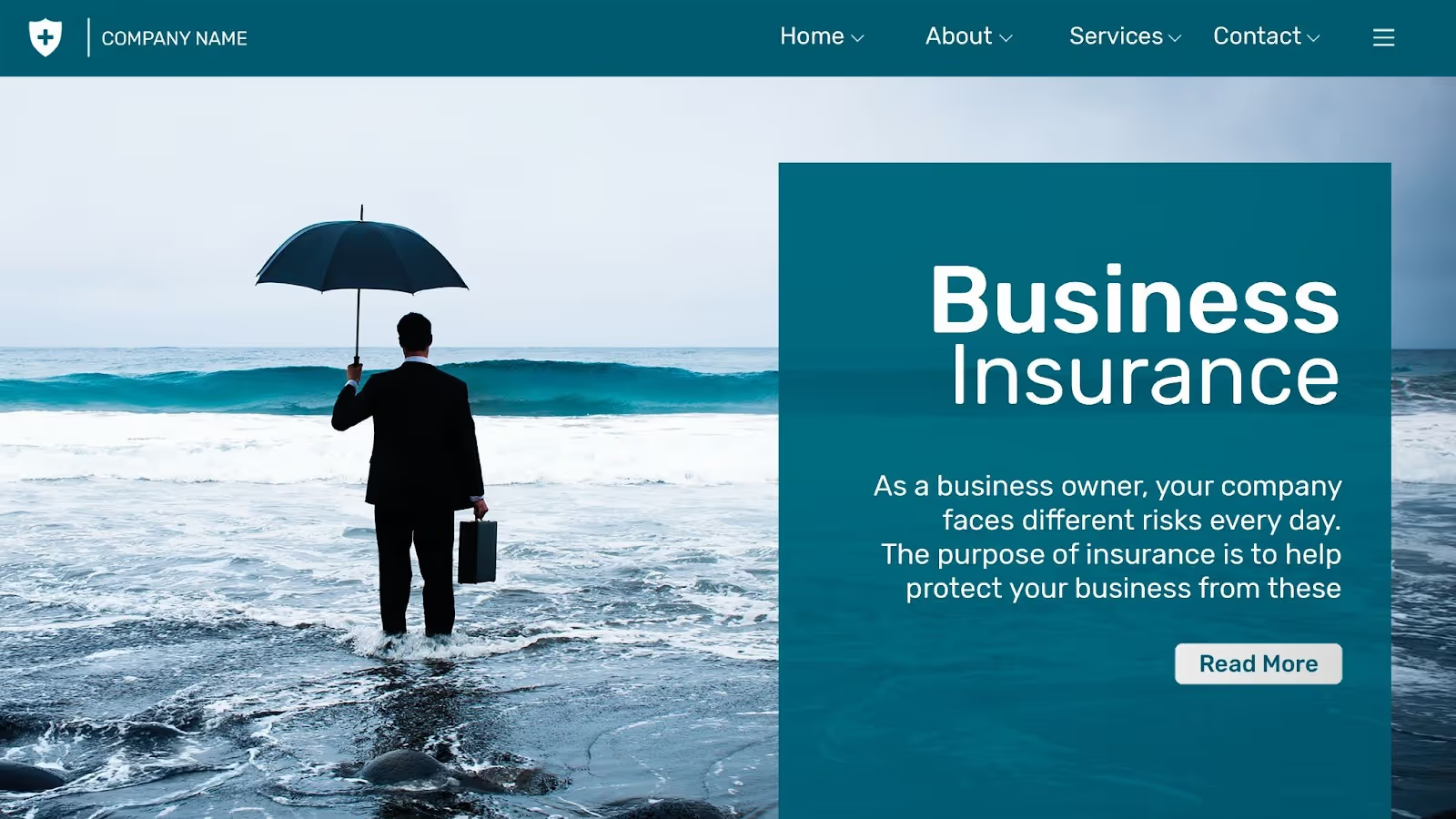

Insurance policies for small businesses are born from the need to protect your assets. The very thought of an imminent or uncertain accident forces us to take out insurance and compensate for possible bad situations.

That’s why you should have a policy that can cover everything that happens.

It doesn't matter how new or how small your business is, it’s almost certain that your business can be affected by a natural disaster, theft, or lawsuits.

That is why we present seven types of insurance policies that you could get for your subject matter expert (SME) to avoid those dangers.

The business insurance policy is the way you use to manage risk to protect your company and yourself from external and internal threats. You can think of it as a shield against different things that life may throw at you, like natural disasters, riots, theft, crisis, and more.

You can use these policies to guard against both financial and physical losses.

When you own business insurance, the liabilities of running a company disappear, or at least are covered by the insurance company. This is a positive situation since there are legal issues that could be enough to close your facilities.

However, choosing small business insurance is not as easy as it may seem, especially if your choices need to pass through different people.

Below you can see what are the steps to follow to buy an insurance policy.

It’s quite simple to purchase an insurance policy for your business.

However, the most important step that you, as a business owner, should take is to choose the insurance policy that best suits the needs of your business. The only way to do this is to know the risks your business might face.

For example, a small business that owns a car should consider vehicle insurance, which can cover their assets in case they suffer any loss or harm. Damages from natural disasters – like floods – vandalism, and other events like this are also included.

On the contrary, if you're a small owner in a low-risk industry – such as consulting, tutoring, dropshipping, and similar – you may be able to lower your premium costs by combining this policy with a General Liability Insurance in a Business Owner's Policy (BOP).

So, if you want to get an insurance policy for your small business, here’s what you need to do according to the U.S. SBA:

If you still haven’t decided which insurance policy applies for your business – or you just don’t trust your agent – we can’t blame you, there are different options, and choosing one above all is a hard task.

However, before you select one, it’s important to note that for other legal factors, you and your company will need to take steps to reduce your risk exposure.

These steps may include:

If you have already done that, below we have covered 7 small business insurance policies that could work for you and your business.

When you hire an employee, you must get a workers' compensation insurance policy from an insurance company. This will cover disabilities, medical treatments, death benefits, and more. All this is in the case that a worker is harmed or killed inside the business’s jurisdiction.

Keep in mind that this is not regular health insurance, but with this sort of service, your business is covered to avoid any lawsuits or bigger issues with your employees.

This is one of the most basic insurances that a business must have. It will protect your company from different claims such as injuries, property damage, medical treatments, personal damage, and more.

It’s a great option for those small entrepreneurs that are starting out but still want to be protected against people with bad intentions or unfortunate situations.

This kind of business insurance policy helps you guard your equipment and property – whether it is rented or owned – that are part of your company.

Remember that while it protects equipment, signage, inventory, and furniture from fire, storm, or theft, this policy doesn’t cover earthquakes or floods. So you may need extra insurance to cover those occurrences.

This business insurance is perfect to protect your project from a disaster that is out of your control. When a catastrophic event like this happens, companies tend to stop their operations until the danger passes.

Until work operations resume, your company will suffer from lost revenue due to the inability of your staff to work in the office, manufacture products, or make sales calls.

This type of insurance policy is especially applicable to companies that require a physical location to make money, such as retail businesses.

You may know them as BOP. This insurance is a combination of general liability insurance with property coverage features. As such, it covers customer injuries, property damage, claims from products, and more.

Since it’s one of the most complete insurances available, it also includes some of the business interruption policy characteristics. The BOP isn’t extended to your employees.

In general, this is a must-have for owners of stores, restaurants, and more.

This insurance is essential for companies that are focused on manufacturing industries to sell them to final consumers. Even a company that has extreme quality control measures and tries to make its products safe may find itself in a lawsuit for damages caused by one of its products.

Whereby, the product liability insurance policy works to protect both small and large businesses, with coverage available to specifically fit a specific type of product.

Since lots of businesses are using cloud technology to store their information, data breach insurance helps you back up this information in case you lose it.

You can use it to pay for some of the services that are used to recover or identify lost/stolen data, such as identity theft monitoring.

If the previous policies aren’t enough, here we share three additional options that you may find interesting.

Most professionals or entrepreneurs start their small businesses in their own homes. Unfortunately, homeowners' policies do not cover home-based businesses in the same way that commercial property insurance does.

Therefore, if you’re operating your business from home, it’s necessary that you request additional insurance from your agent to cover your work equipment and all your inventory in the event of a problem.

Professional liability insurance, also known as errors and omissions (E&O) insurance, covers any business against negligence claims or lawsuits due to damages resulting from errors or non-compliance.

It should be noted that there are no single policies for professional liability insurance, so each industry has its own set of concerns that will be addressed in a custom policy written by the insurance company for your business.

If your business uses vehicles to move people or merchandise, or even puts the vehicle to some other use, they should be fully secured to protect businesses from liabilities.

At a minimum, businesses should protect themselves against third-party injuries, but a full insurance policy will also include that vehicle in the case of an accident. If employees use their own cars to drive during their workday, their own personal insurance policy will cover them in the event of an accident or in case of fatalities.

Selecting the right insurance for your small business is not an easy task, especially after reading all the options you have above.

However, if you're not sure which direction to take, work with an insurance broker – also called an agent – to compare coverage options and find the perfect provider for your needs.

If you’re not into brokers, you can also use an online insurance marketplace to choose providers and compare quotes instantly.

Keep in mind that insurance policies are rarely one-size-fits-all for your business. This is why you may need to bundle a group of policies together to create the perfect coverage plan for your company.

Some policies come prepackaged; for example, the general liability insurance policy is often combined with the business property insurance policy, creating a “Business Owners Policy (BOP)."

When you look for insurance bundles, you can get the coverage you need at a lower cost than you were to get them separately.

If your company has an adequate insurance policy in your industry, you’re going to be accountable and responsible for any legal situation. After all, a reliable and responsible insurance company can respond in the event of a catastrophe or event with your business.

In addition, don’t be afraid of changing your policy if you’re growing faster than expected, your equipment is your asset and they need to be covered.

According to the HSE report, “in 2020/2021, an estimated 441,000 workers sustained non-fatal injuries according to self-reports.”

These small business insurance policies address your basic exposures and can help you – and your employees – to avoid being part of the number of statistics. However, you will likely need additional coverage depending on your industry, location, and the product you’re developing.

Fortunately, businesses have access to a wide range of insurance types to protect against these types of perils. Your company can avoid a huge financial loss or even avoid bankruptcy just by making the right decisions at the right time.

Of course, this is also an international requirement when you work with people. For example, most international laws require businesses to carry workers' compensation insurance if they have employees. Similarly, all company-owned vehicles must have commercial auto insurance.

Any business that engages in high-risk activities – such as construction – must have an adequate insurance policy. Otherwise, you run a serious risk of bankruptcy in the event of lawsuits against the company.

Additionally, a liability insurance policy may be required for any job in which the worker performs. So, be sure to talk to a business insurance professional to ensure you have the coverage your business will need.

Anthony Martin is the founder, CEO, and owner of Choice Mutual. He has been a licensed insurance agent since 2010. Currently, Anthony holds an active insurance license in all 50 US states, including DC.

.avif)

%20(1)%20(1).avif)